Setting boundaries with your finances is a good way to protect your mental and financial well-being, as well as your relationships with the people in your life. Should you fail to set financial boundaries and have the ability to politely decline requests, you may find yourself overextended emotionally and financially.

If you want to maintain pleasant and healthy relationships with friends, family, and partners, Here’s the tips on how to set and keep financial boundaries.

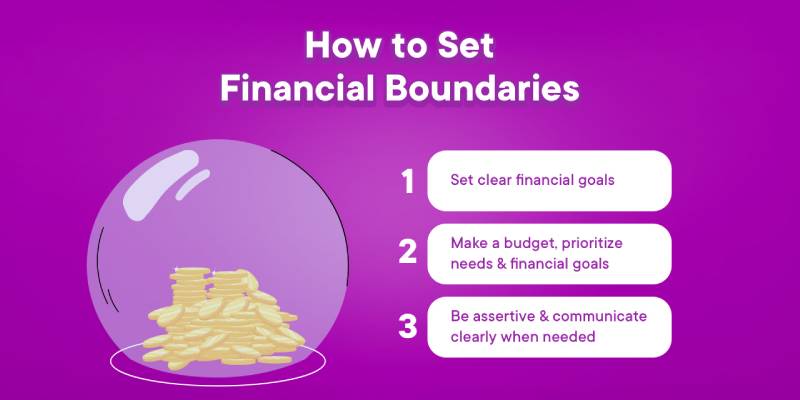

Set reasonable expectations and goals.

Prior to setting financial boundaries, it’s essential to identify your financial goals.

Making short-term and long-term goals for your goals could be helpful. Next, organize them according to importance so that you may take more concrete action. Priority tasks like setting up an emergency fund or paying off credit card debt are an excellent place to start. Though they might not always come first, longer-term objectives like investing for the education of future generations might still be considered.

Setting and maintaining these goals can help you maintain your financial boundaries and facilitate communication with others.

To track spending and make sure you’re achieving your goals, budgeting apps are a terrific resource. Couples can manage their finances more openly and make better long-term plans by connecting their credit cards and bank accounts to the Honeydue app, for instance. Along with features like bill payment reminders and monthly spending limitations by category, the app is available for download for free.

Prioritize your own financial needs

According to a Federal Reserve research from May 2023, a third of adults who are living with their parents between the ages of 22 and 24 do so in order to provide them with financial support; this number rises as adults become older. While providing for your friends and family financially is a great goal, you also need to be honest about your own financial need.

In response to the study, about 40% of adults stated that they couldn’t use their cash resources to pay for a $400 emergency. In addition to hurting your present self, putting extra financial strain on yourself can also keep your future self from being able to assist others after you’ve achieved greater financial stability.

Before you think about giving money as a gift, make sure your finances are in order. Investing your money in a certificate of deposit (CD) or high-yield savings account can be an almost risk-free strategy to grow your wealth. With APYs of 5% or above, many of Select’s top-rated high-yield savings accounts—like Lending Club High-Yield Savings—offer rates that are far higher than the 0.47% average savings rate for the country.

Set rules around lending money

Consider carefully before lending money to others, especially if it is done out of shame or pressure, just as you would when giving money to loved ones.

It’s hazardous to lend money to friends and family since it could strain your bonds. Conflicts may arise regarding the amount loaned, the terms of repayment, failure to pay, and other problems.

If you decide to lend money, be sure to establish ground rules that both parties understand and accept, such as the total amount and the timetable for revenge.

Lending money should only be done so in amounts that you can afford to lose. You don’t want to find yourself able to pay your own bills because you are reliant on the money you have been loaned.

Share your boundaries with others

Establishing boundaries with friends, family, and significant others requires open communication.

58% of Millennials and 57% of Generation Z dispute with their spouses over money, per a Bread Financial survey conducted in February 2023. This isn’t always a terrible thing because a strong, long-term relationship requires having difficult money conversations.

When discussing your financial goals with a spouse, Wendy Wright, a finance and marriage therapist, previously advised to keep an open mind. “Without judging them and without doing the math, just put them on there so that each person is allowed to dream.”

Depending on who you are discussing your money with, you may or may not be more or less transparent about them. Talk openly and truthfully with your loved ones about money.

Make an effort to become more at ease with saying no. This might be as simple as declining to go out to dinner or as complex as paying for a trip.

Giving your loved ones context might make them more appreciative of your viewpoint and forgiving of your boundaries.

summary

Long-term mental and financial well-being depend on setting up reasonable boundaries when it comes to your cash. It’s possible to increase your comfort level in setting and maintaining financial boundaries by having an open line of communication and establishing realistic goals.

- Top 5 Health Insurance Stocks to Add to Your Portfolio - July 26, 2024

- 7 Reasons Edamame is Great for Your Health - July 26, 2024

- 2024 Paris Olympics: How Many US Athletes Are Competing? - July 26, 2024